A bit about the trouble in Italy but, as almost always for me, more interest in the lessons for Latvia.

Being in the Eurozone provides 1) predictability about inflation – the European Central Bank’s primary task is price stability, defined as close to but below 2% inflation, which 2) makes wage setting and setting of interest rates much easier. 3) Using the same currency has advantages for firms (no transaction costs from exchanging from one currency to another and no exchange rate risk when performing exports and imports) as well as for individuals – it is e.g. super-practical to have the same currency in all three Baltic countries.

But 4) the Eurozone does NOT in and by itself create economic growth – this is still an issue for economic policy of the individual countries.

And, crucially, 5) having abandoned one’s own currency in favour of the common currency, a country can no longer print its way out of fiscal trouble.

Italy did not pay much attention to 4) and 5) and now faces the consequences.

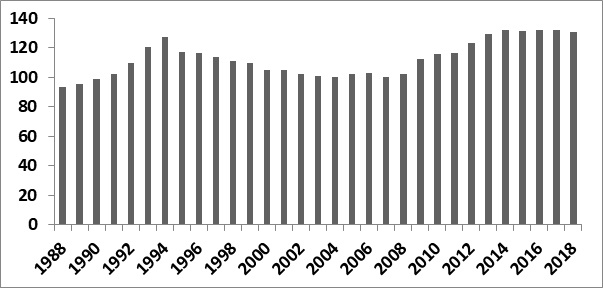

The country entered the Eurozone in 1999 with a debt level already above the 60% stipulated by the Maastricht criteria, see Figure 1. This was possible due to the elasticity of that criterion – countries could be admitted with debt above 60% if this ratio was coming down “sufficiently fast”. As Figure 1 also shows, this was not the case in Italy where the level has actually grown again in the past decade and now stands at 131% of GDP, equivalent to about 2 trillion EUR or around 70 years of Latvian GDP, no less.

Figure 1: Italy’s government gross debt as a share of GDP, 1988 – 2018

Source: IMF

But why such a dismal performance?

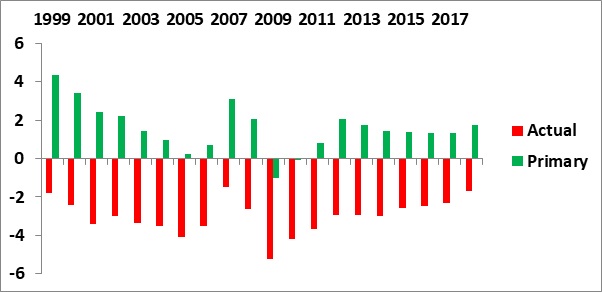

It is actually not really because of overly profligate fiscal policy. Yes, Italy routinely runs budget deficits, see Figure 2 (the columns in red). But had it not been for interest payments on its vast debt, its budget would in most years show budget surpluses (the green columns; primary budget balance is the difference between revenue and spending when interest payments are excluded.).

Figure 2: Actual budget balance and primary budget balance, % of GDP, Italy, 1999 – 2018

Source: IMF

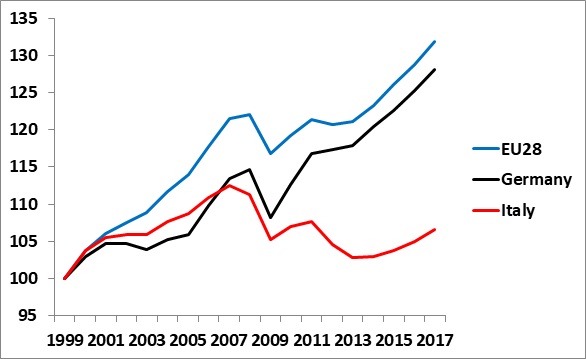

Italy’s continuous debt build-up is much more due to a phenomenally poor growth performance since joining the Eurozone, see Figure 3. Italy’s economy is just a dismal 6% bigger in 2018 than it was in 1999 – two lost decades! Germany has grown 28% since 1999 (and Latvia, by comparison, 94%).

This reflects non-observance of point 4) – Italy has failed to make its economy more efficient, more competitive, less bureaucratic etc. Germany was the sick man of Europe in the early 1990s but transformed its economy with the Hartz IV reforms. Italy must also act but hasn’t done so for two decades. And now it retorts to the usual blame-game: It is the fault of Germany, of the EU Commission etc. Pathetic!

Figure 3: Index for GDP performance since the inception of the Eurozone. EU28, Germany and Italy. 1999 = 100

Source: Eurostat and own calculations

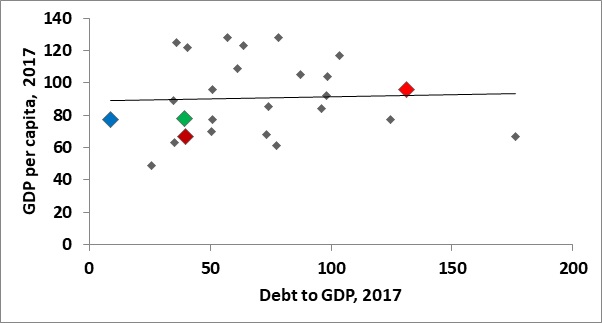

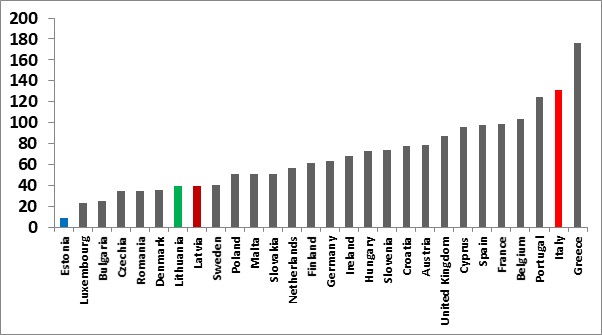

Italy would like the EU Commission to allow a larger budget deficit in order to stimulate the economy but isn’t that pursuing a strategy that has already failed? Fiscal stimulus, especially when targeting long-term growth, can be very beneficial but data does not seem to suggest that that has been much done in Italy, see Figure 4. Higher accumulation of debt does not make countries richer (the regression line is about as flat as it can be) and many countries with low debts are among the richest in the EU. Figure 5 provides the current debt-to-GDP numbers for all of the EU countries for comparisons to be made.

Figure 4: GDP per capita against debt to GDP, 2017, EU28 minus Luxembourg and Ireland. EU average GDP per capita = 100. Estonia, Latvia, Lithuania, Italy highlighted.

Source: Eurostat

Note: Luxembourg and Ireland omitted due to their misleading GDP figures. Inclusion, however, would not change the picture.

Figure 5: Debt to GDP, %, 2017, EU28

Source: Eurostat

The task at hand is thus to make the economy more competitive, more attractive to invest in, less bureaucratic etc. – what we usually refer to as ‘structural reforms’ – and here is a country that really needs it! The past 20 years are best described as utter economic failure.

Italians are angry but they should be angry with their own politicians – and the most angry should be young people. Think back to Figure 2. The difference between green and red is currently about four percentage points. This is what tax payers have to cough up annually for many failed fiscal policies in the past – this is what young people have to pay for, from now and decades into the future.

Latvia’s debt burden is much, much smaller (Figure 4) and thus a similar burden is not presented to the young people of this country. Moreover, Latvia has also been much better at pursuing growth than Italy has. Good!

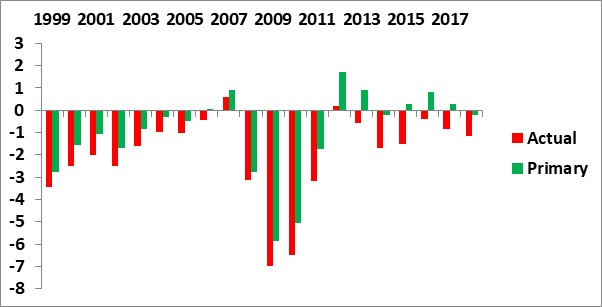

That said; I can still be a bit worried when witnessing, after eight years of growth and very low unemployment, a fiscal policy that nevertheless aims at a budget deficit. Latvia is not Italy but it is just not proper fiscal policy to, at the top of the business cycle, aim at a budget deficit. For comparison, the similar figure to Figure 2 for Italy is shown in Figure 6 for Latvia.

Figure 6: Actual budget balance and primary budget balance, % of GDP, Latvia, 1999 – 2018

Source: IMF

One wonders if the financial crisis is now so far in the past that the lessons from it – among many things to avoid pro-cyclical fiscal policy – are being, if not forgotten, then taken less seriously?

Morten Hansen is Head of the Economics Department at Stockholm School of Economics in Riga and a member of the Fiscal Discipline Council.

Points of view expressed here are not necessarily those of the Fiscal Discipline Council.

Komentāri (3)

Sskaisle 04.12.2018. 11.42

Eiropa gatavojas jaunai finanšu krīzei …

nu Latvijā nav ko gatavoties – te shēmas , kā dzelzceļa sliedes – nabagiem atņems, bagātajiem pieliks –

https://www.focus.de/politik/experten/gastbeitrag-von-gabor-steingart-meldung-vom-04-12-2018_id_10017757.html

0

Sskaisle 04.12.2018. 11.25

priekš manis skaitu par daudz, to es nespēju …

bet par Itāliju – tā tomēr ir tāda baigākā liecība -šorīt ziņās klausos – ka kāda tur vadoņa – premjera Kontes vai – tēvs izrādās arī savā firmā nodarbinājis strādniekus bez līguma nemaksajot valstij nodokļus. It kā jau nekas ipašs , bet visa tā itāļu ģimenīte – populisti esot zvērējuši sabiedrībai, ka ir tīrāki par kristāla gabaliņiem –

melo visi – patiešām visi –

vēl – lasu, ka itāļi sper zemes gaisā un spļauj melnu – cik Brisele ir ļauna un ES slikta – tai pat laikā – itāļi aizņemot vislielāko procentu daļu EK birokrātijā, tas Draghi ir ECB vadītajs, Mogerīni vada ārlietas, Tajani parlamentu

klau – un tad itāļiem nav kauna kritizēt ES?

Jā …. tik netaisna, tik negodīga ir pasaule …..

0

Sskaisle 04.12.2018. 11.29

kas attiecas uz Latviju – Mortensens laikam arī ar naivumu sists – vai izliekas

šī valsts – Latvija – ir jau pašos neatkarības atjaunošanas pirmsākumos izveidojusies par čekistu – komunistu pašapkalpošanās biroju – kur sabiedrības intereses ir tikai sauklis – tikai ietinamais papīrs beztiesiskuma uzvarai

0