We are used to the tiresome East-West divide in terms of GDP per capita – the fact that the eastern European countries of the EU are still poorer than most of their western European compatriots.

Increasingly, however, it is worth thinking (also) in terms of a North-South divide. The financial crisis and its aftermath has seen strongly diverging developments in the north of the EU vis-à-vis the south and I try to illustrate that with a couple of graphs. These diverging developments should be worrisome for the future of the EU and not least the future of the Eurozone.

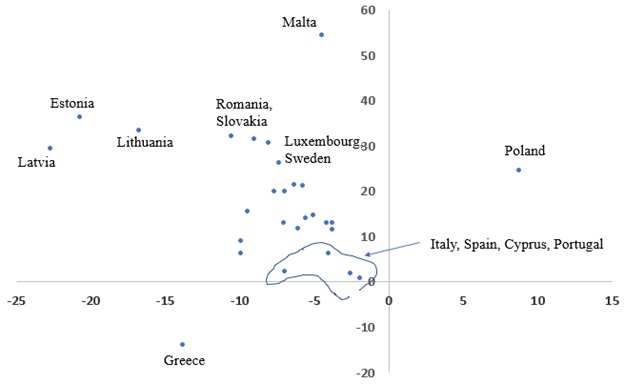

In Figure 1 I try to compare the GDP development during the crisis (1st axis) with the GDP development after the crisis (2nd axis). As we know, the Baltic countries took the biggest hit during the crisis (= far to the left on the 1st axis) – with Latvia hit the hardest – but all three have also made strong comebacks (= high up on the 2nd axis). Other strong performers in this way are e.g. Romania and Slovakia as well as Malta and Luxembourg (in both cases influx of population have helped) and Sweden (some will say due to their floating exchange rate). Poland is in a class of its own with growth during the crisis (i.e. no crisis due to no credit boom in the first place) and growth afterwards.

But what really stands out, negatively, is the development of the EU’s southern countries. Italy, Spain, Portugal and Cyprus were hit at varying degrees during the financial crisis but have barely, with the slight exception of Spain, grown since the end of the crisis more than seven years ago. Clear failure!

And Greece is a tragedy completely in its own class – massive recession during the crisis, massive recession after the crisis; or, in Greece’s case; crisis followed by crisis in altogether by now some ten years. A country that does not in any way or form fit into the Eurozone but could need a new currency, big devaluation, debt forgiveness etc.?! I don’t think it will happen but it is strange to see a country willingly enduring so much economic pain for so long.

Figure 1: GDP change, peak to trough during the financial crisis, 1st axis, GDP change trough through 2017, 2nd axis; percentage points, EU28 minus Ireland (see Note 3)

Source: Eurostat and own calculations

Note 1: Peak to trough varies but is roughly 2007 – 2010 for all countries.

Note 2: Poland was the only EU country not to suffer a recession during the financial crisis so here the periods are simply 2007 – 2010 and 2010 – 2017.

Note 3: Ireland is excluded due to major changes to its GDP calculations.

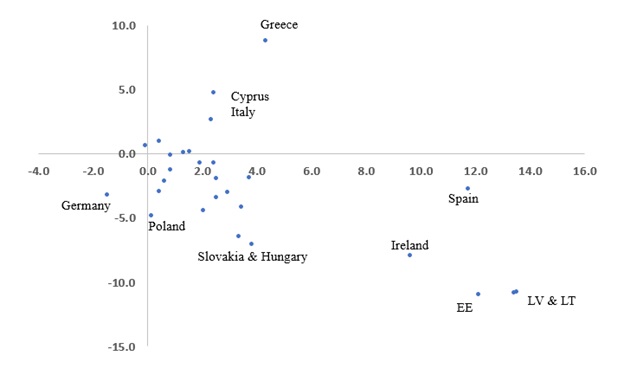

Another way to illustrate this development is to look at change in unemployment instead of change in GDP. This is done in Figure 2 where, once again, we see the Baltic countries clustered together, this time far to the right on the 1st axis (= unemployment exploded during the crisis) but also far down on the 2nd axis (= unemployment has declined substantially after the crisis).

Baltic exceptionalism, if you will.

Ireland has a similar experience, albeit not so pronounced. But again southern Europe disappoints: Spain saw its unemployment rate soar during the crisis but it has come down only minimally since. Cyprus and Italy are even worse with unemployment growing during the crisis period but continuing to grow afterwards – and also here Greece is in a non-enviable league of its own with unemployment rising rapidly under and after the crisis period of 2007 – 2010.

Economically, a failed state to my mind.

Not surprisingly Poland also stands out here – unemployment grew just a tad in 2007 – 2010 and has then declined some five percentage points since then.

But the country that has been the main beneficiary of the Eurozone is Germany. The country did not see a credit boom in 2007 – 2010; was still hit by the crisis in terms of GDP due to loss of exports but still saw its unemployment rate decline during the crisis as well as afterwards with its increasing cost competitiveness.

Hardliners would claim that it is Germany that does not fit into the Eurozone by being über-competitive vis-à-vis its trading partners. Expect tension to resurface as southern countries find it hard to increase competitiveness vis-à-vis Germany and thus must live with high unemployment for the foreseeable future.

All in all: Very uneven development in the EU and Eurozone.

Figure 2: Unemployment change 2007 – 2010 (1st axis), unemployment change 2010 – 2017 (2nd axis); percentage points, EU28

Source: Eurostat and own calculations

An extra note on Baltic unemployment rates: They have come down a lot due to more employment after the crisis (good) but also due to poor demographics (bad) as well as migration (good and bad). Purists will see migration as entirely bad – for me, I strongly prefer that Baltic unemployment could find jobs elsewhere instead of staying unemployed in the Baltics. It alleviates what would have be a big short-run problem (how to handle these many unemployed and their bleak future prospects – I don’t want to think about young Greeks who have already been unemployed for several years; they may be part of a generation that never really gets into the labour market). But of course migration is not just a long-run issue; it is THE long-run issue (together with demographics) and here lies the main policy failure of the unsustainable boom of 2004 – 2007: It sowed the seeds for the big bust and the ensuing outward migration.

That said, the Baltic countries, with their bounce-back in terms of growth and unemployment reduction, fit very well into the Eurozone and are very – very! – different cases from the southern countries of Greece, Italy, Spain, Portugal and Cyprus.

Morten Hansen is Head of Economics Department at Stockholm School of Economics in Riga and a member of the Fiscal Discipline Council of Latvia.

Opinions expressed here are not necessarily those of the Fiscal Discipline Council.

Pagaidām nav neviena komentāra